Introduction

When borrowing money from a bank or financial institution, one of the most important distinctions borrowers encounter is whether a loan is secured or unsecured. This classification affects how the loan is approved, what responsibilities the borrower has, and how risk is managed by both parties.

In many lending situations, insurance is also involved to provide an additional layer of protection for lenders and borrowers. As a result, the concepts of secured insurance loans and unsecured insurance loans emerge. While these terms may sound complex, they are straightforward once you understand how collateral and insurance work together.

This article explains secured and unsecured insurance loans in a clear, beginner-friendly manner, highlighting their differences and providing practical examples using American names for better understanding.

What Is a Secured Insurance Loan?

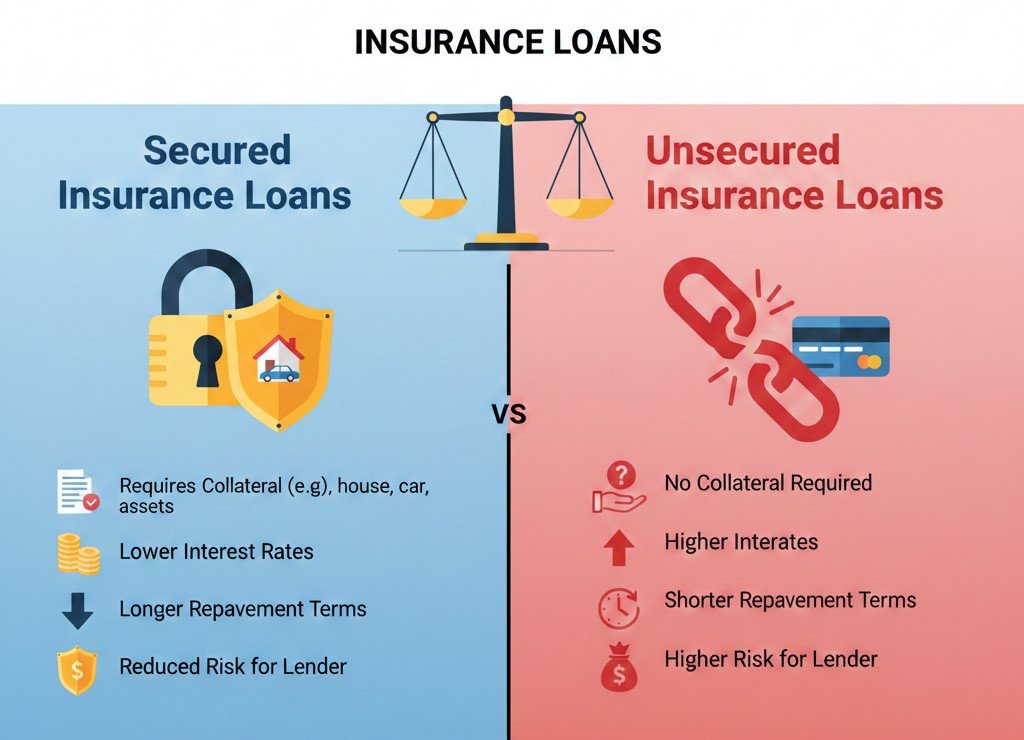

A secured insurance loan is a loan backed by collateral — an asset that the borrower pledges to the lender as security. In addition to the collateral, insurance coverage is often attached to protect the asset or loan balance from unexpected events.

Collateral reduces the lender’s risk because the asset can be claimed if the borrower fails to repay the loan. Insurance adds another protective layer by addressing risks such as damage, loss, disability, or death.

Common characteristics

-

Requires collateral such as a house, vehicle, or savings account

-

Insurance may cover the asset or loan balance

-

Typically used for larger or long-term loans

-

Offers structured risk management for both lender and borrower

Example: Mortgage with insurance

David purchases a home using a mortgage loan. The property itself serves as collateral for the loan, making it a secured loan. Additionally, David obtains mortgage protection insurance.

If David encounters an event covered by the policy, the insurance may assist with loan payments or balance settlement. Meanwhile, the lender retains security through the property.

This combination of collateral and insurance represents a secured insurance loan structure.

What Is an Unsecured Insurance Loan?

An unsecured insurance loan is a loan that does not require collateral. Approval is typically based on factors such as income, credit history, and repayment capacity rather than asset ownership.

Even though collateral is absent, borrowers may still choose or be offered loan insurance to protect repayment obligations under specific circumstances.

Common characteristics

-

No collateral required

-

Approval relies on borrower profile

-

Insurance focuses on repayment protection rather than asset coverage

-

Often used for personal expenses or smaller borrowing needs

Example: Personal loan with credit life insurance

Jessica takes a personal loan to cover wedding expenses. The loan does not require any asset as security, making it unsecured. However, Jessica opts for credit life insurance linked to the loan.

If an event covered by the policy occurs, the insurance helps settle the outstanding balance. While there is no collateral involved, the insurance provides repayment protection, creating an unsecured insurance loan scenario.

How Collateral and Insurance Work Together

How Collateral and Insurance Work Together

To understand the difference more clearly, it helps to separate two components:

Collateral

Collateral is a physical or financial asset pledged to secure repayment. It represents a lender’s fallback if repayment fails.

Examples include:

-

Real estate

-

Vehicles

-

Fixed deposits

-

Investment accounts

Insurance

Insurance is a contractual arrangement that addresses defined risks affecting repayment or assets. Instead of seizing assets, insurance responds by providing financial support when covered events occur.

In secured loans, insurance often protects the collateral itself. In unsecured loans, insurance mainly protects repayment obligations.

Key Differences Between Secured and Unsecured Insurance Loans

1. Presence of collateral

The most fundamental difference lies in collateral requirements.

-

Secured insurance loans involve asset backing.

-

Unsecured insurance loans rely solely on borrower credibility.

2. Risk distribution

In secured loans, risk is distributed between collateral and insurance coverage. In unsecured loans, insurance becomes a primary structured protection since no asset is pledged.

3. Loan purpose

Secured loans are commonly associated with asset acquisition, such as homes or vehicles. Unsecured loans are more frequently used for flexible purposes like education, travel, or personal expenses.

4. Insurance role

Insurance in secured loans may protect both the asset and repayment. In unsecured loans, insurance typically focuses only on repayment continuity.

Real-Life Comparison Example

Secured scenario

Robert takes an auto loan to purchase a car. The vehicle serves as collateral, and he also obtains vehicle and loan protection insurance. If the car is damaged or an event affects repayment, insurance coverage may apply while the lender retains security through the vehicle.

Unsecured scenario

Amanda obtains a medical expense loan without pledging assets. She chooses loan protection insurance to safeguard repayment responsibilities. The lender does not hold collateral but benefits from insurance-linked risk mitigation.

These examples highlight how collateral presence fundamentally distinguishes secured and unsecured insurance loans.

Advantages of Secured Insurance Loans

Asset-based borrowing access

Borrowers can leverage owned assets to obtain financing.

Structured risk framework

Collateral and insurance together create layered protection.

Support for larger financing needs

Secured loans are often associated with substantial borrowing amounts tied to asset purchases.

Advantages of Unsecured Insurance Loans

Advantages of Unsecured Insurance Loans

Accessibility without assets

Borrowers can obtain financing without property ownership.

Simplified borrowing process

Absence of collateral reduces documentation related to asset valuation.

Flexible usage

Funds may be applied to a wide range of personal or professional purposes.

Situations Where Secured Insurance Loans Are Common

-

Home purchase financing

-

Vehicle financing

-

Business equipment loans

-

Savings-backed borrowing

In these cases, the financed asset itself frequently becomes collateral.

Situations Where Unsecured Insurance Loans Are Common

-

Personal expense financing

-

Education loans without collateral

-

Medical expense funding

-

Short-term personal borrowing

Here, borrowing is linked more to financial profile than asset ownership.

Considerations Before Choosing Between Them

Evaluate asset availability

Ownership of acceptable collateral influences secured loan eligibility.

Understand insurance coverage scope

Insurance terms vary depending on policy type and loan structure.

Assess financial stability

Income consistency and repayment capacity shape unsecured loan access.

Review loan purpose

Asset-based purchases may naturally align with secured loans.

Clarify obligations

Understanding responsibilities under both structures supports informed borrowing decisions.

Common Misunderstandings

Insurance does not replace collateral

Some borrowers assume insurance eliminates collateral requirements. In reality, collateral and insurance serve different functions.

Unsecured does not mean unprotected

Although unsecured loans lack collateral, insurance can still provide structured repayment protection.

Secured loans are not risk-free

Even with collateral and insurance, borrowers remain responsible for loan agreements.